Mortgage rates have fallen in the last few weeks – but what about long-term rates? Where are rates headed in the next five years, and should you wait for mortgage rates to drop before buying or refinancing? The mortgage interest rate is determined by several factors, all of which can give us clues about the future.

One of the most important indicators for predicting mortgage rates is the yield on the 10-year US Treasury note. Mortgage rates and 10-year Treasury yields typically move in the same direction, although mortgage rates are often higher because lenders take on more risks. This difference between the two is known as the spread, and we’ll account for that when we measure where mortgage rates can go.

With that in mind, the first step is to look at where economists believe Treasury yields are headed over the next five years. To create a forecast, we will combine economists’ forecasts with data compiled using artificial intelligence.

Michael Wolf, global economist at Deloitte Touche Tohmatsu Ltd., outlined the outlook for Treasury firms over the next five years in the December update from the Deloitte Global Economics Research Institute.

“We assume the Fed leaves rates unchanged until December 2026. The federal funds rate reaches a neutral 3.125% in mid-2027,” he wrote. Wolf said that the yield on the 10-year Treasury will gradually decrease until the second quarter of 2027, “staying at 3.9% from the third quarter of 2027 until the end of 2030.”

Let’s mark that prediction.

Some estimates point to relatively high long-term yields. For example, analysts at Goldman Sachs expect the 10-year Treasury to rise over the long term to 4.5% by 2035.

Meanwhile, the Congressional Budget Office (CBO) projects that the yield on the 10-year Treasury will reach 4.1% by the end of 2026, rising gradually to 4.3% in 2030.

Anthropic’s Claude artificial intelligence compiled its predictions into a consensus forecast, which we’ll use below.

Read more: Why did interest rates increase after the Federal Reserve cut?

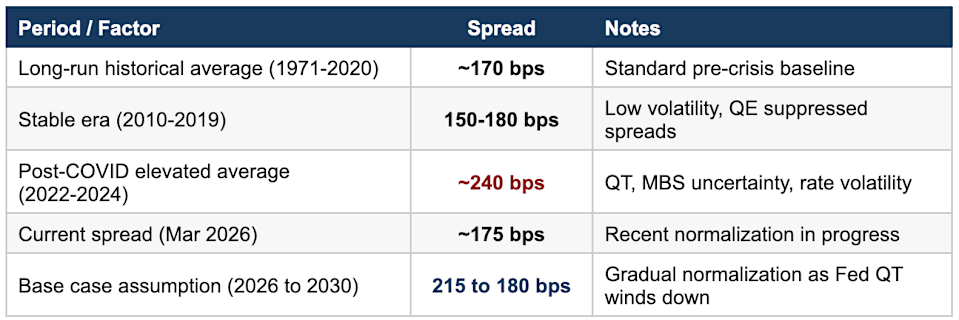

As mentioned, the 10-year Treasury and 30-year fixed rates are separated by the spread. The difference between the two has been on either side of 2.5 percent in recent years. That’s a big change compared to the spread from 2010 to 2020, when it was less than two percent — and usually closer to 1.5.

Using a 2-percentage-point spread, here’s an example of how Treasurys and bond rates compare:

10-year Treasury Rate = 4%

Spread = 2 percentage points

Mortgage = 6%

Here’s a recent example: As of March 5, the 10-year Treasury yield was 4.09%, and the 30-year mortgage rate was 6.00%. The distribution was 6.00 – 4.09 = 1.91 percentage points.

The spread is less than two percent, which is another reason that mortgage rates have decreased.

Claude AI suggested using a different compressed slow release:

“The spread between the 30-year fixed-rate mortgage and the 10-year Treasury is driven by prepayment risk, credit risk, and the supply/demand of mortgage-backed securities (MBS). The Federal Reserve’s quantitative tightening (QT) program has extended the spread after 2022 as private equity markets expand. It is expected to continue to tighten.”

Using these published estimates, we can now complete a five-year mortgage rate forecast.

Using the Treasury forecast, we include the case suggested by Claude that assumes a spread between the bond market and 30-year fixed rates to accumulate a five-year forecast:

Read more: When will mortgage rates go back to 6%?

While this forecast is for a base case with a gradual expansion trend, easing inflation, and moderate Fed monetary policy, Claude AI also prepared a “bull” forecast and a “bear” forecast:

A bull’s-eye: easy crouching

“The Fed has managed to guide inflation back to 2% without a sharp drop. The FOMC rate gradually decreases in 2027 pulling the 10-year yields to 3.3% as the time premium compresses”. 2030.”

The bear case: persistent inflation and financial stress

“Inflation is holding steady above 2.5% and rising US Treasury deficits are pushing up the high-term rate, keeping the 10-year yield close to 4.4 to 4.6%. Spread widens to 240 bps due to market volatility and heavy MBS supply in secondary markets. Mortgage rates rise to 7.020% before 6% to 6% by 2030.”

Of course, these are long-term estimates based on historical trends and broad expectations. All of these numbers can be thrown out the window if one of the following happens:

-

10-year bonds are either overperforming or underperforming. For example, the yield can fall in the economy, such as a recession, or the rise of increasing government deficits.

-

The spread between Treasurys and mortgage rates is narrowing – or widening significantly.

-

Monetary policy, as conducted by the Federal Reserve, is highly variable.

No forecast predicts a 3% mortgage rate in the next five years. However, who saw such low mortgage rates around the corner in 2007 when rates were about where they are now? Things like the Great Recession and global pandemics are rarely on the radar, and such extreme events are all it takes to drive mortgage rates into the cellar.

The analysis above predicts that 2027 mortgage rates are close to 6%.

Based on the above estimates, mortgage rates are not expected to drop significantly in the next five years. However, a recession or other unknown disruption to the economy (such as a financial crisis or other pandemic) can change the outlook.

If you’re considering an adjustable rate mortgage with a fixed first term, you’ll first consider how long you’ll be living in the home you’re financing. Then the long term mortgage forecasting begins. The best way is to choose the first time that best fits your current budget.

Read more: 8 strategies to get a low mortgage rate

#Credit #rate #forecasts #years #experts #predict