Source: JP Morgan via Marketwatch

In normal times, about 20 percent of the world’s oil production passes through the Strait of Hormuz. That flow has been cut off except for Iranian oil and a few other ships that the Iranians allow through. This disruption has led to a significant increase in oil prices in the future:

Source: Business Economy

But this price rise has been speculative, driven by the (reasonable) expectation of future shortages rather than current oil shortages. In fact, until now the delivery to markets around the world has not slowed down, because sending oil from the Persian Gulf to major markets takes 4-6 weeks. As a result, there was already a lot of oil in the sea, outside the Strait, when the war started.

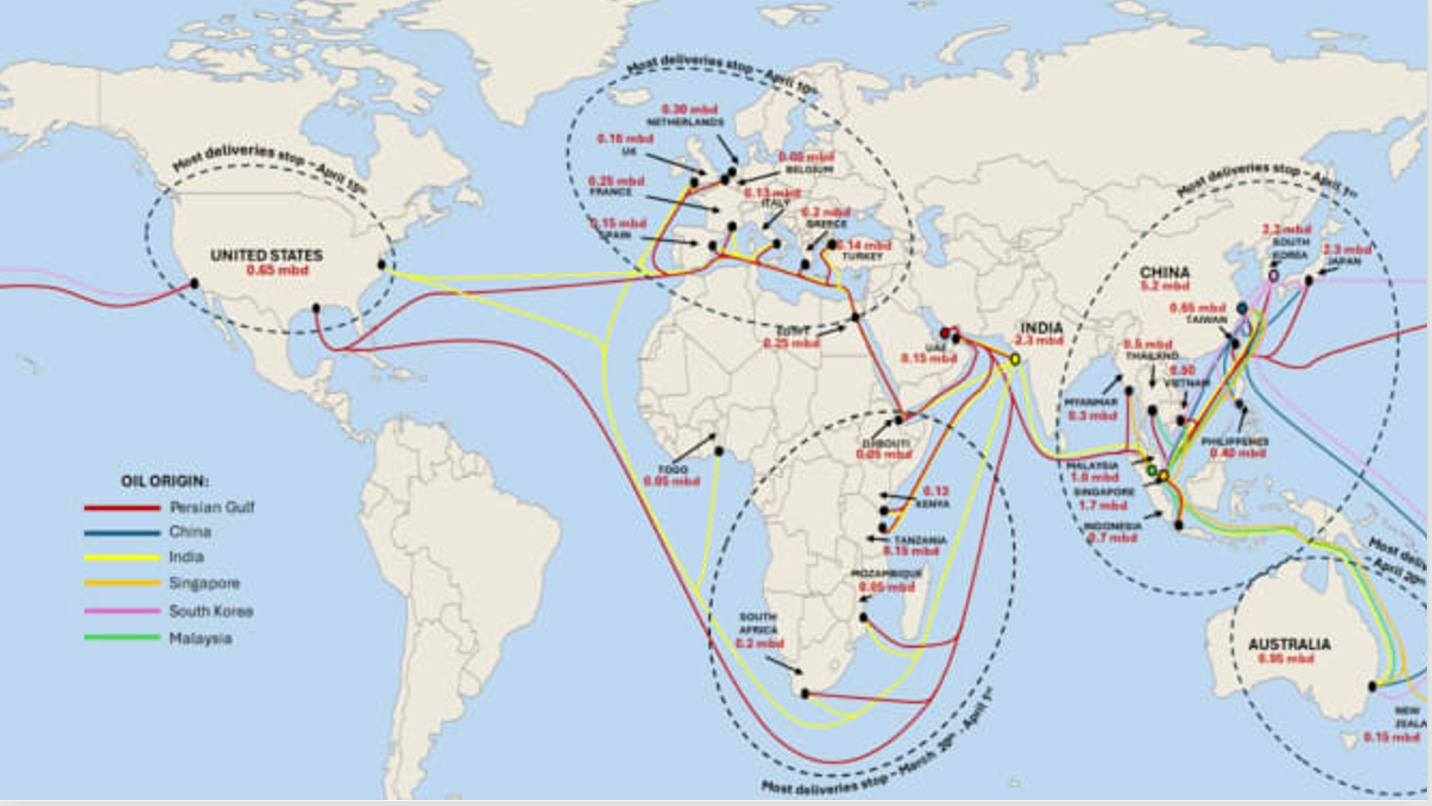

However, this grace period is about to end. The oil crisis is about to get worse. The map at the top of this post shows JP Morgan’s estimates of when tankers from the Gulf will stop arriving at various locations. Shipping to Asian markets will end this week; delivery to Europe will end next week.

And once the crisis hits, there will be no more room for jawboning in the markets. Since the start of the war there have been several times that Donald Trump has been able to lower prices by ensuring that meaningful negotiations are ongoing. his invisible friends the Iranian regime, but that won’t work once the oil runs out. So prices will have to rise to any level that destroys demand enough to match the available supply.

PS: The United States buys little oil from the Persian Gulf, but we can expect US oil prices to rise due to global shortages.

So how high will oil prices go? I have written about this before, but I thought it would be useful to update the analysis, highlighting the uncertainty of expectations and the real danger of very high prices.

There are two main sources of uncertainty. The first is that we don’t know how much oil will be able to escape the Gulf. Oil supplies are now much reduced, but not by the full 20 million barrels of oil per day that used to flow through the Strait of Hormuz. The Saudis have a pipeline that allows them to send some of their oil to the Red Sea; Oman has a pipeline that transports oil around the Strait. And Iran is still allowing millions of barrels of its oil to pass through. Whether all this “leaking” will continue depends on the course of the war.

Second, how much must prices rise to reduce the given quantity demanded? We know from past oil shocks that the price elasticity of demand for crude oil is low – that is, even a large increase in price causes a small decrease in demand. But in the current crisis it is important How that easy decline, a number that it is impossible to estimate with any precision, really is.

So what is a reasonable range of possibilities? I have considered three conditions for oil supply disruption: a “low disruption” level where supply is reduced “only” 8 percent from normal levels, a medium level where supply falls 12 percent, and a high level of disruption where it falls 16 percent. I have also considered three criteria for the price value of oil demand: “high” at 0.2, medium at 0.15, and less than 0.1.

And I think that without this war, the price of Brent would be about $65 a barrel. In that case, I get the following matrix:

Readers should know that Robin Brooks made a similar analysis in the opinion. My numbers, however, are even more alarming – and I believe yours should be afraid

In particular, by presenting the analysis in this way, I run the risk of conveying the impression that we should take a moderate, intermediate / intermediate result. That is not a safe idea at all.

In fact, what would it take to get to my “high distraction” level? This is what could happen if Iran’s oil supplies are cut off, allegedly by the US attack on Kharg Island, and if the pipeline supply is disrupted by Iran’s retaliation against other Gulf oil facilities as well as Houthis’ attacks on Red Sea vessels. That is not something that can happen. In fact, that’s what we should expect if the Trump administration follows through on what appear to be current war plans.

And if oil really goes to $200 or more, it is very easy to imagine a complete crisis of the world economy, with inflation and recession.

Since the start of this fight I have noticed a sharp division of opinion among scholars. Economists and economists were relatively bullish about our ability to weather this storm. But talk to or read about energy experts – people who focus on the physical side of the oil problem – and their hair is on fire.

I am usually a macroeconomist. But my hair is starting to smoke.

MINOPE KODA

I’m sorry

#problem #oil #close #body