Weekly Examiner, March 30, 2026

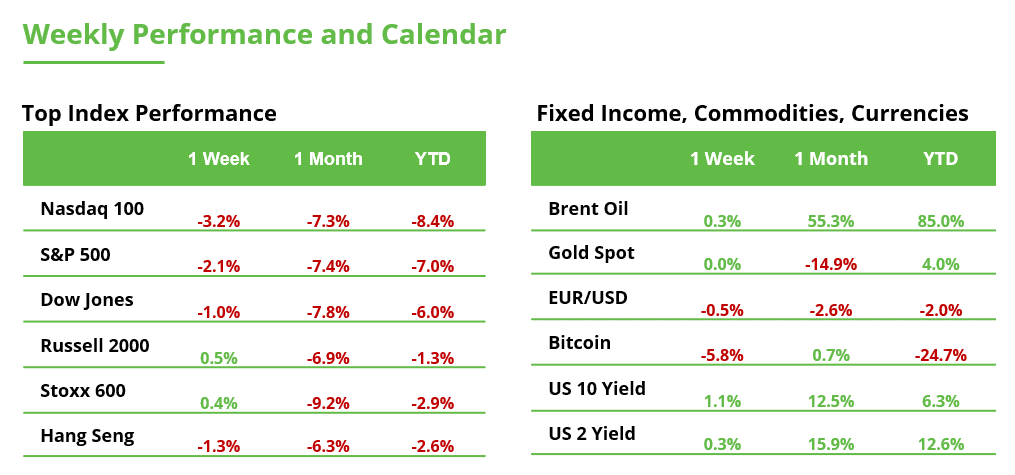

Last week loss indicates a weak market condition that is increasing as major pressures begin to build. Although investors are focused on the price from high energy prices, the biggest risk is the impact of global growth if prices remain high. There are already early signs that high energy costs are beginning to weigh on demand in parts of the global economy, confirming this fact.

Markets often respond to this change with sentiment first. Investors are more cautious and don’t want to pay high prices for stocks, which means that markets can fall even before the company’s earnings are meaningfully affected. This helps explain why the near-term risk of financial markets is much lower in terms of a sharp drop in earnings, and higher in terms of return on investment.

Conditions are already showing this awareness.

There has been a lack of aggressive call buying, indicating that investors are not yet confident enough to chase higher. At the same time, the need to put (security) remains strong. Simply put, investors are preparing for risks rather than positioning for a strong rally.

This is also reflected in volatility. Daily market movements are still in place, but options markets continue to price in high risk. This gap suggests that even though the markets are not broken, they are still aware of surprising surprises, especially if high energy prices start to weigh heavily on demand.

Investment Benefits for Retail Investors

1. Stay invested, but take a more balanced approach

Markets are under pressure, yet they are not broken. This supports you to stay invested, but avoid taking too much risk. Focus on maintaining a balanced distribution rather than increasing exposure during this time.

2. Don’t chase security, create stability

Security has become expensive in the stock market. Instead of responding:

- Stay invested in companies with stable earnings

- Limit exposure to speculative, high-quality brands

- Focus on variety and gradual positioning

- Avoid emotional decisions driven by headlines

3. Add hedges to your portfolio

Investment Takeaway: Markets are not in a state of panic, however, they are getting worse. Investors are now taking a more safe stance, with risks ranging from inflation alone to broader concerns about growth and sentiment.

For retail investors, this is not the time to bet boldly. It’s time for discipline, discretion, and balanced portfolio construction.

Gold Stumbles, But Long-Term Case Holds

Gold’s recent volatility doesn’t mean its role as a safe haven has been broken, but it does challenge the way investors think. In our view, the recent sell-off reflects the volatility of the public sector rather than fundamental changes. After the strong rally, gold has been largely dominated by investors in ETFs, trading and derivatives, which has left it vulnerable to volatility as the dollar strengthens and rate expectations change.

That being said, gold is not a hedge. During times of market stress, it may initially fall as investors raise capital and reduce risk, especially when positions are extended. This can give the impression that it is “failing” as a habitat, when in fact it is behaving like a water reservoir in a stressed system.

The drivers below are always solid. Central bank purchases, continued diversification away from fiat currencies, and political uncertainty continue to support demand. However, the latest action highlights that gold is a long-term hedge, not a short-term investment.

For investors, the takeaway is that gold still plays a role in portfolios, but the expectations surrounding its behavior should be realistic.

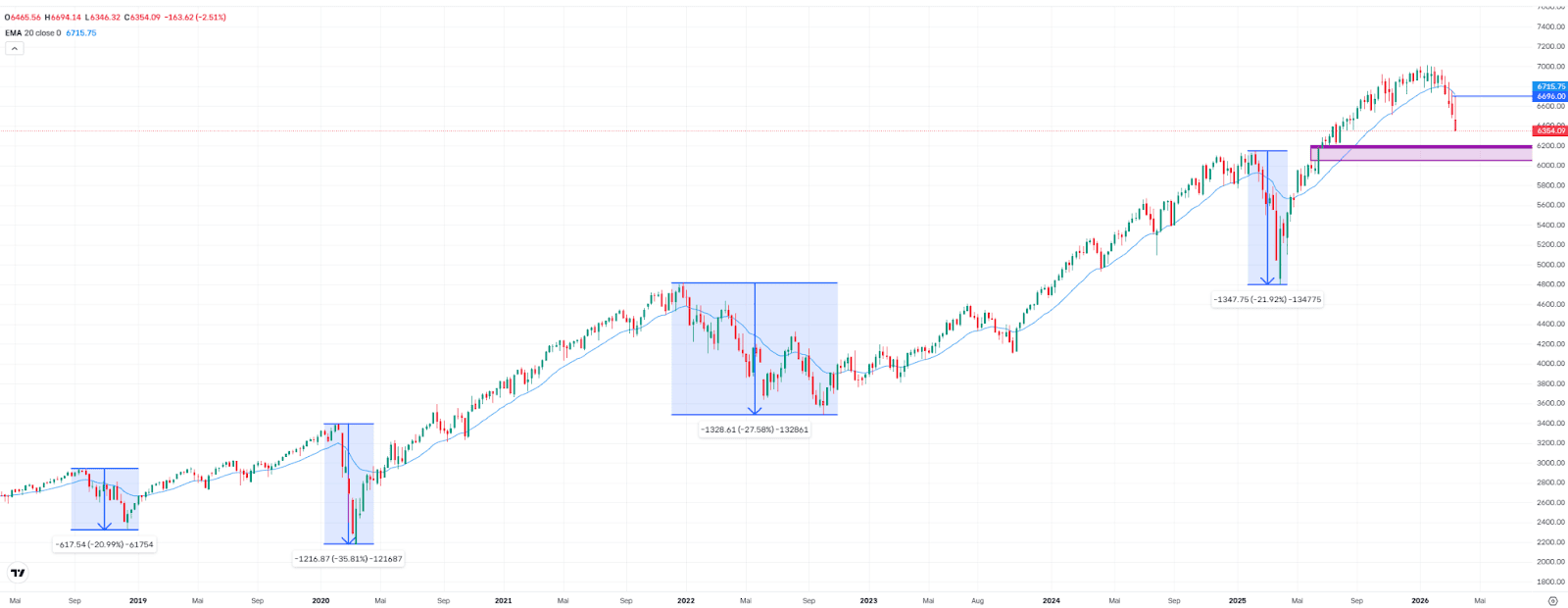

S&P 500 Approaches Correction Zone

The S&P 500 fell another 2.5% last week, marking its fifth straight week of losses. The index is now more than 9% below its record high. A 10% drop is considered an adjustment by law. Such pullbacks usually occur once a year, while large drops of 20% or more tend to occur every few years (see chart). The causes may vary, but currently the conflict in the Middle East is driving a clear sense of de-escalation. Looking at history, markets have repeatedly recovered and continued to reach new highs. Currently, the S&P 500 is only approaching correction territory.

At such low levels, so-called positive value gaps are often tested, which can serve as potential support areas. The next is between 6,187 and 6,201 points, followed by another between 6,050 and 6,173. This does not mean that these conditions must be met, but the possibility has increased in recent weeks. A short-term trend usually begins with a move up to a recent high. This would require an all-time high last week at 6,694 points, as well as a move back above the 20-week moving average, which sits just above that level. Until then, the risk of another low remains high.

S&P 500, weekly chart. Source: eToro

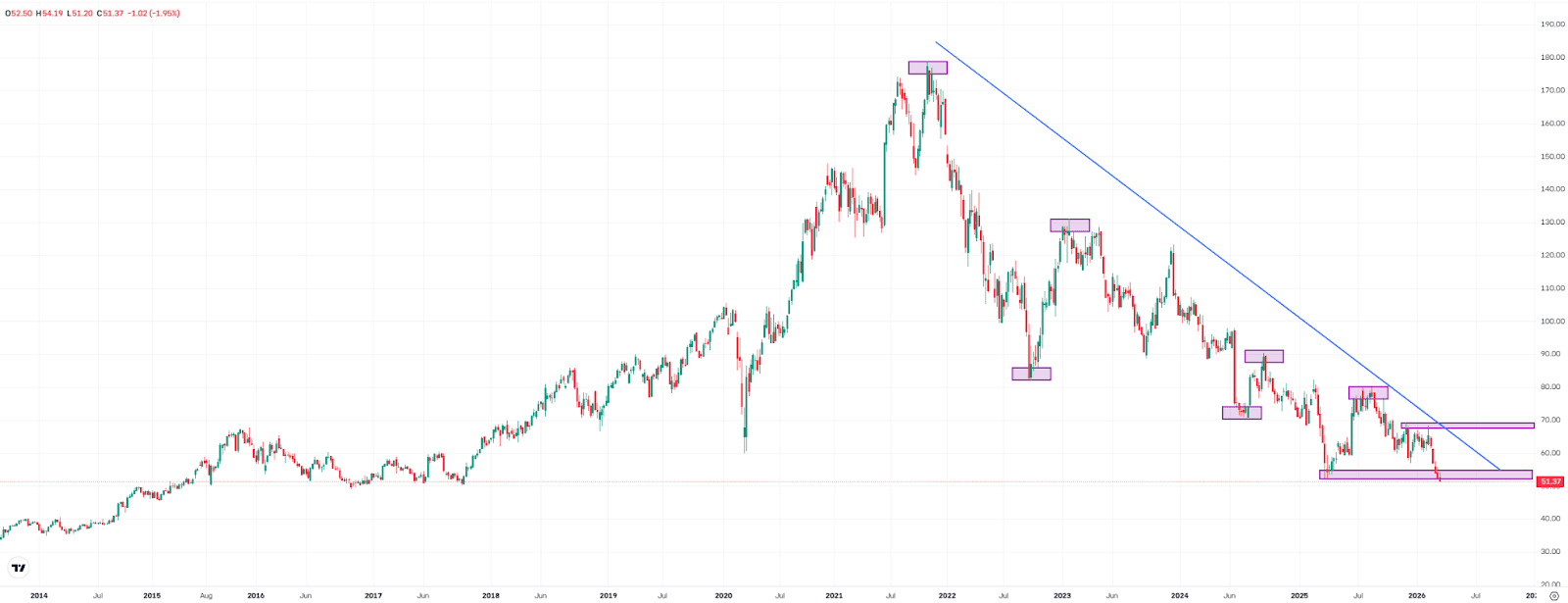

Nike Under Pressure

Shares of Nike are down about 19% this year. Last week, the stock closed another 1.9% lower at $51.37, which shows its lowest level since 2017. This puts the company on track for the fifth consecutive year of losses. Overall, the stock is down more than 70% from its record high. For now, the main goal is to prevent another selloff. Buyers are pushing against a long-term downtrend.

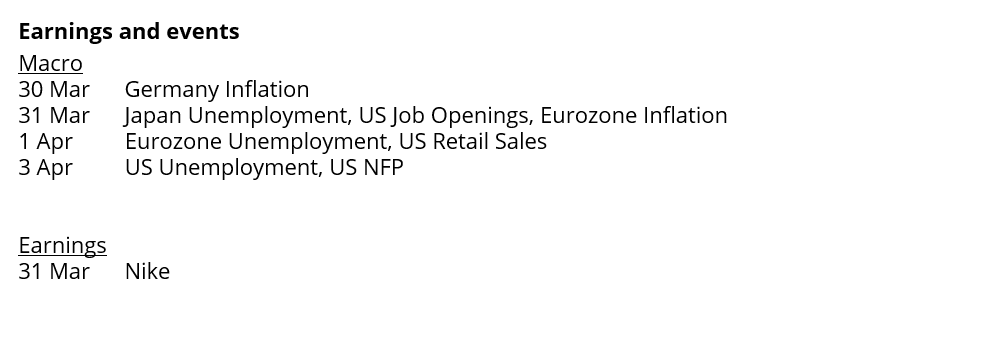

To break the pattern of lows and lows (see chart), the stock would need to retrace the double high it made in February around $68. Without this explosion, there is no new way to ascend. A period of stability followed by recovery can at least improve the short-term outlook. Any signs of a slowdown in the Middle East could also lift market sentiment quickly. Investors are looking to Tuesday evening’s earnings release for clear signs of the company’s outlook.

Nike, weekly chart. Source: eToro

Bitcoin Has Support as Markets Turn Defensive

Bitcoin has a key support of $65K after a weekly correction. The rule above 55% ensures a protective environment where the housing houses funds in BTC instead of circulating in altcoins. Volumes contract as “Fear & Greed Show” drops below 15 again.

On-chain information is always mixed. Retailers (<10 BTC) ba bokella ka tekanyo ea beke le beke. Li-whale (> 1000 BTC) are traded in rebounds. ETFs record a negative weekly flow that breaks the previous monthly trend.

Macro pressures that do not yield BTC yields with high real yields, strong dollar and geopolitical carry trades. Excessive pessimism opens the door for smart bounces. The market does not resolve this tension, buying it at 65-75K USD laterals.

Integration is no longer optional, it’s on the move. Nasdaq and the New York Stock Exchange are adding cryptocurrencies to market infrastructure, from clearing to derivatives, while Fannie Mae is experimenting with bitcoin as loan collateral.

As traditional currencies put crypto on its rails, the direction of the price may remain unstable, but the direction of the system is not. The next part of the market will be built within this convention.

This communication is for informational and educational purposes only and should not be construed as investment advice, your recommendation, or offer of, or solicitation to buy or sell, any financial instruments. This information has been prepared without regard to the particular recipient’s investment plans or financial situation and has not been prepared in accordance with legal and regulatory requirements to promote independent research. Any representation of the past or future performance of a financial instrument, index or investment product is not, and should not be considered, a reliable indication of future results. eToro makes no representations and assumes no liability as to the accuracy or completeness of the content of this publication.

#Markets #Pressure #Growth #Risks #Increase #Weekly #Examiner #March