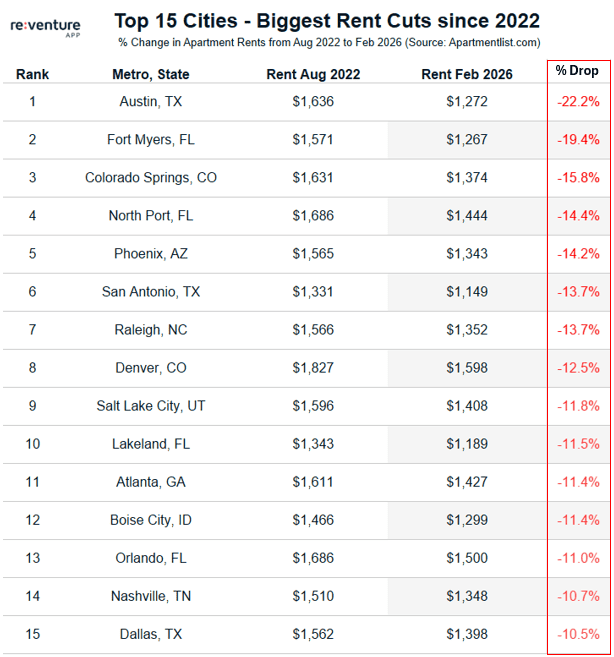

There seems to have been a change in vibe in the US housing market over the past six months. What started in places like Austin, Texas with falling rents and home prices, seems to have spread to other parts of the country. As you can see in the table below, Austin isn’t the only one with double-digit rents decrease from 2022:

And what happened to the rental market appears to be happening to home prices as well. A survey from the Residential Club shows that 75% of the largest metro areas in the US have seen it the adjusted home price is reduced last year.

But will this trend continue? And what can we expect from US housing in the next few years? Let’s dig inside.

Payments are no longer a problem

When it comes to housing in the US, the first thing we need to address is affordability. After all, if people can’t afford homes, they don’t.

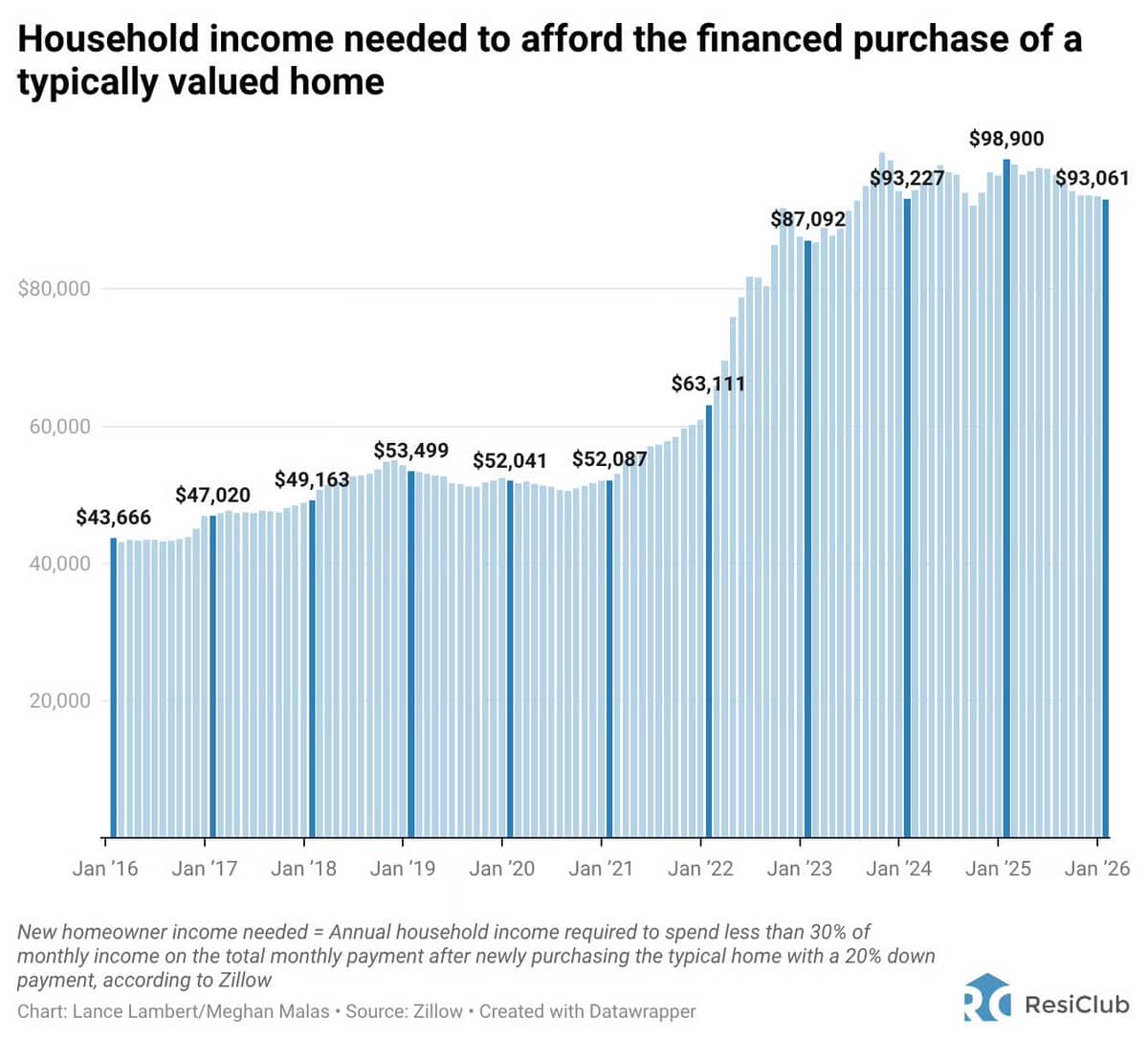

The biggest issue with affordability, as you already know, is that incomes haven’t risen in line with mortgage rates. In fact, you need about twice as much money today to buy a typical US home compared to before COVID:

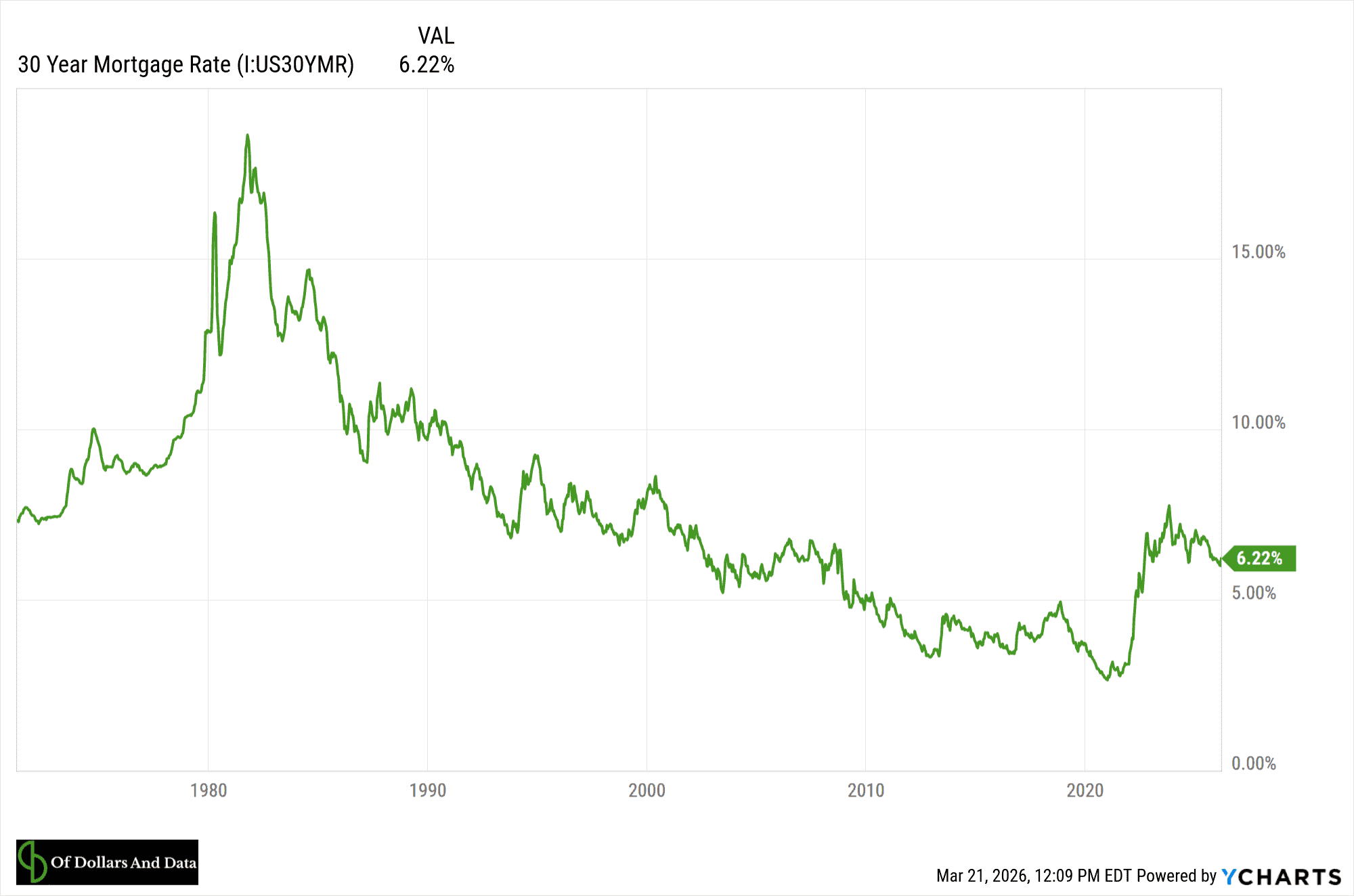

Part of the problem is that 30-year mortgage rates have doubled since early 2020. But, 30-year mortgage rates were tough. outside (on the lower side) from 2010 to the early 2020s:

So to see them returning to their historic tradition today is not that surprising.

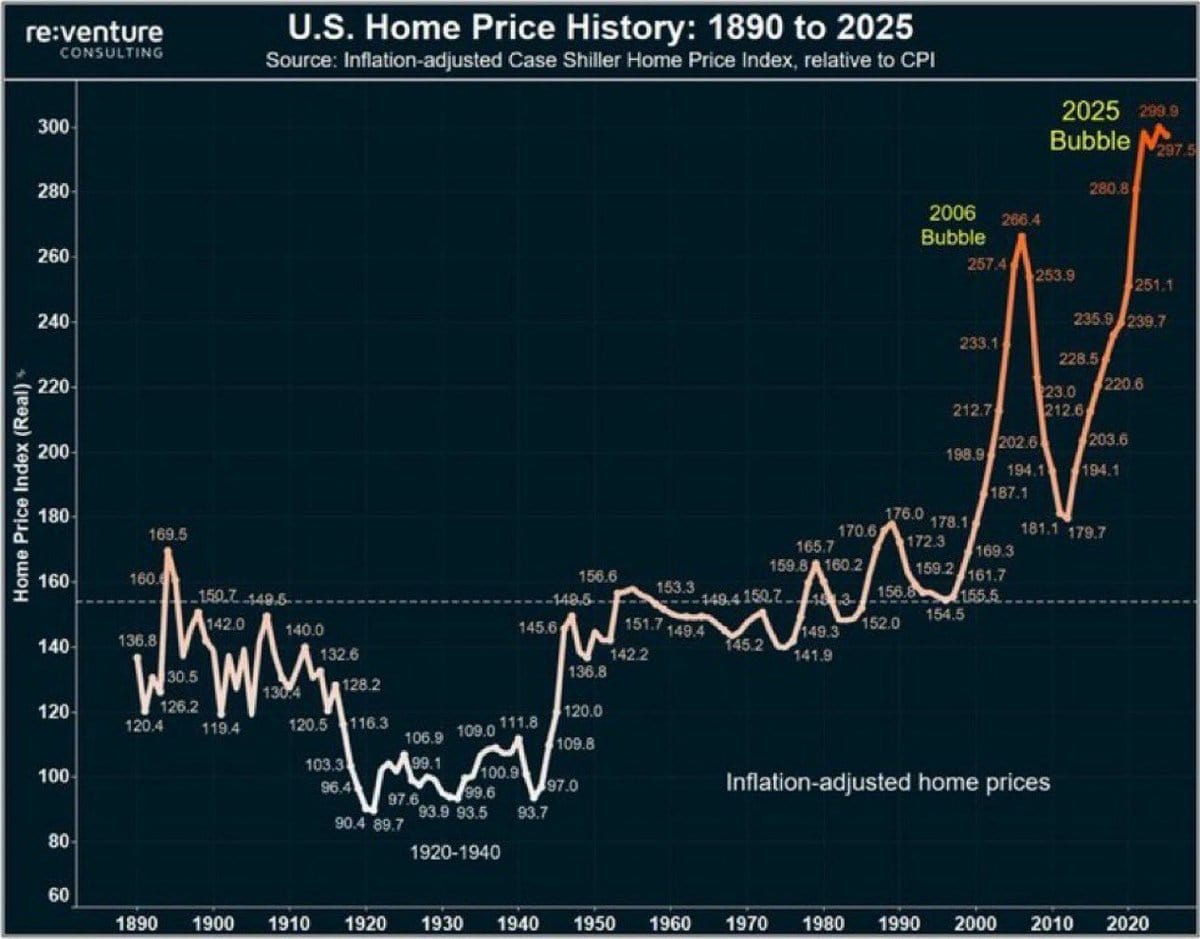

But what not yet returned to its historical norm? Prices.

As the chart below shows, the inflation-adjusted Case Shiller Home Price Index is higher today than it was during the 2000s Housing Bubble:

This suggests that, all else being equal, prices are the problem, not tariffs.

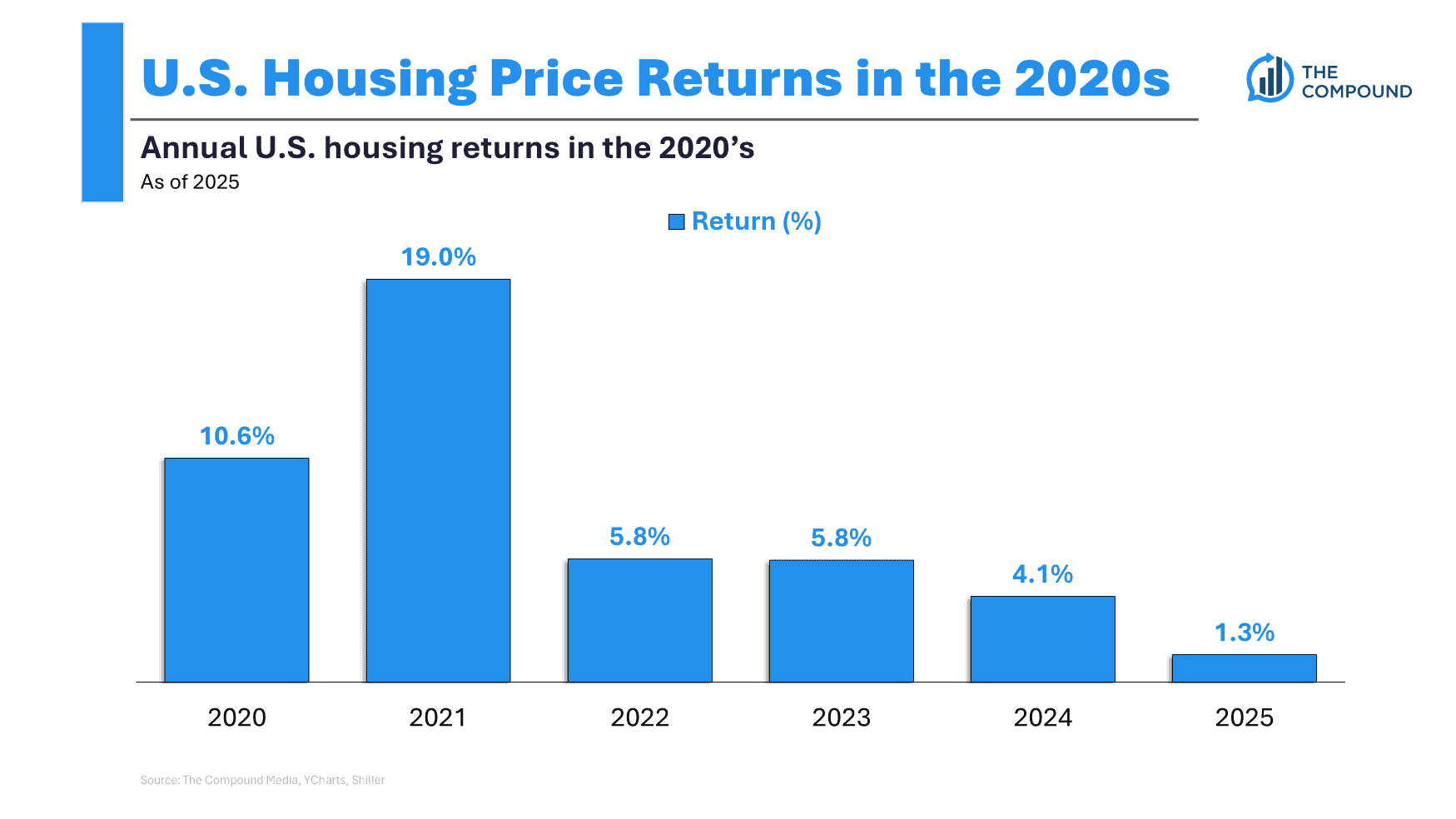

Fortunately for home buyers, prices have started to drop (even down in real terms) over the past few years. You can see this by looking at the year the name US housing prices from 2020-2025 (h/t Ben Carlson):

US housing saw negative returns (after inflation) in 2025. This may be the beginning again. As Reuters recently reported, new home sales fell 17.6% in January 2026, the lowest level since October 2022.

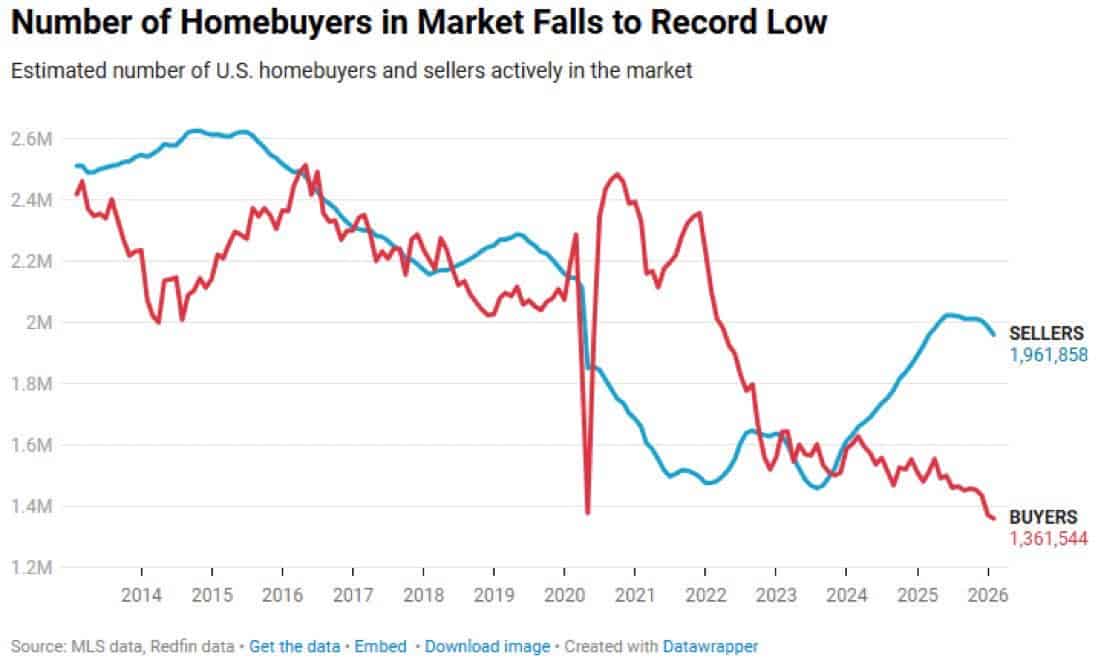

This happens when the number of people buying a home in the market hits an all-time low:

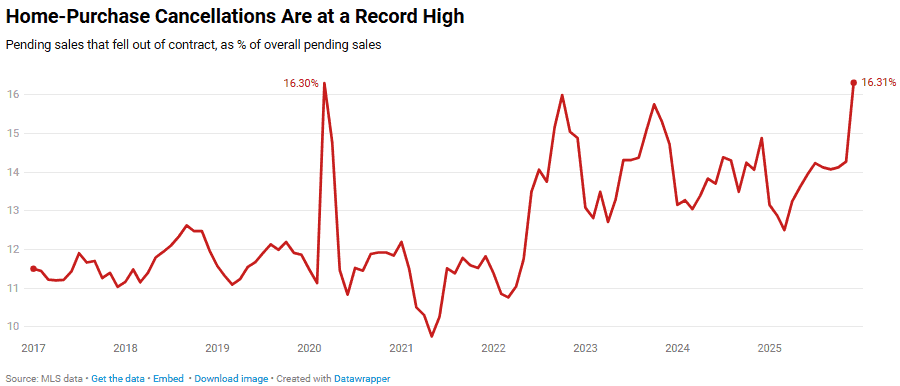

And when home price cancellations reach their peak:

People don’t buy, or even think about buying, when prices start to fall.

And I believe that prices can continue to go down for one simple reason – home equity.

There’s a Place to Fall

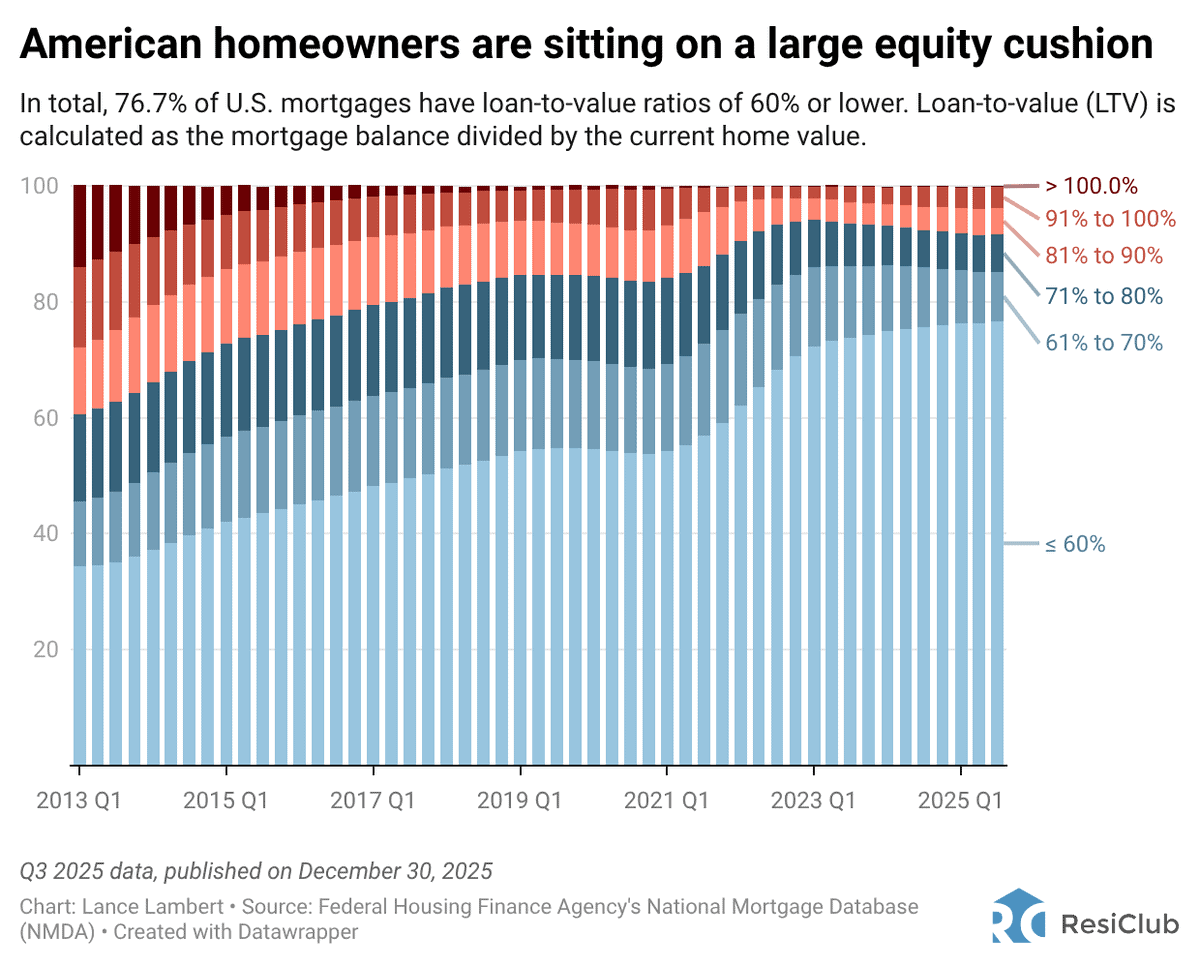

The main reason why housing prices can continue to fall is that homeowners have report home equity situation:

And a good part of the home equity was created over the past few years (as the chart above shows). As a result, homeowners will not feel the pain of home prices falling as badly as they used to. We can prove this with a simple example.

Imagine you bought a house for $100,000 (and all houses cost $100,000). Now imagine that all home prices double to $200,000. Did you find anything? As for non-homeowners, you have. But as far as other homeowners are concerned, you are no different. If you sell your $200,000 house and buy another one, it will cost you $200,000. Nothing gained, nothing lost.

Now assume that all home prices drop to $175,000. Have you lost anything? As for homeowners, you haven’t. You sell your $175,000 home and buy another one for the same price.

This is a simplified version of what happened to US homeowners over the past few years. They got a lot of home equity (in booths) that didn’t translate into a real difference in their lives. So, if local equity were to decrease somewhat (in general), there would be very little impact on them. Without thinking about what they could have had (aka selling higher), they haven’t lost much.

But there is another side to this. Homeowners with large equity cushions may be able to lower their prices and still make a profit. This is happening it can happen that they lower their price compared to someone with less equity.

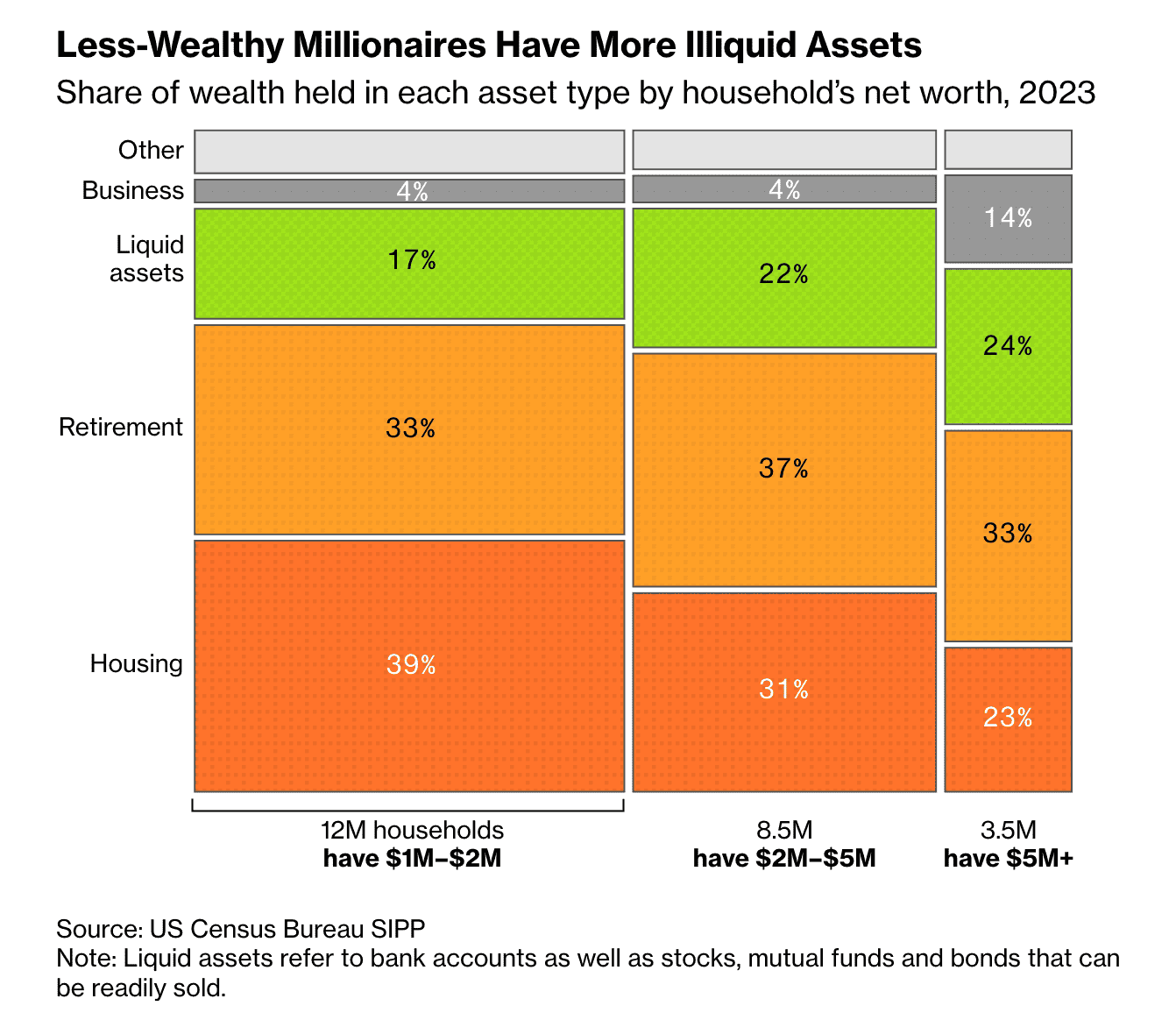

However, it will not feel in that way. Mainly because houses make up a large part of the total wealth. Among US households with $1M-$5M, housing accounts for about 30%-40% of their income:

As a result, most of these families will fight tooth and nail to hold on to home equity, even if only on paper.

Of course, this assumes that these homeowners have the luxury of holding. If the economy collapses and people are forced to sell—because of job losses or other financial problems—equity levels are even less relevant.

However, this battle will be played out over the next few years.

Housing Is Still Slow…And Home

I don’t claim to be an expert on US housing, but one thing I do know is that home prices move more slowly than other asset classes. Even though US stocks fell in March 2009 (during the Global Financial Crisis), US housing did not fall until 2012, more than 3 years later.

I suspect the same thing will happen to US housing in the next few years. Why? Because it will take time for people to renew their beliefs and face the truth. They will need to accept that their home is not selling because of the listing description, photos, or their agent. Not for sale due to price. Once this becomes common knowledge, then the US housing market will begin to pick up again.

Of course, this will not happen everywhere. In San Francisco and New Jersey (my market), I have seen recent examples where families were getting higher rates and selling. up ask. These areas may not experience the same “change of faith” that the rest of the country may be going through.

No matter what happens, the housing market is always in your area. This is the most important thing to remember as a home buyer (or seller) soon. Housing is a complex asset class where averages can hide what’s really going on. For example, one area may see prices fall while another nearby remains strong.

That’s why you have to do your homework and understand your target market. I am generally not a fan of market timing when it comes to buying income generating assets. But when it comes to housing (which I consider good), price is very important. Not only can it be the biggest financial decision of your life, but it is a different choice at the time.

So, do your homework, stay informed, and commit. If you’re a buyer, time is on your side for the first time in years.

Thanks for reading!

If you liked this post, consider signing up for my newsletter.

This is post 496. Any code I linked to this post can be found here with similar numbers: https://github.com/nmaggiulli/of-dollars-and-data

#Homes #Starting #Collapse