China’s steel industry is in critical condition. As the world’s largest iron ore producer and exporter, this sector has a major role in China’s national carbonation process and the development of world iron ore markets.

In September 2020, China announced its commitment to raise carbon dioxide emissions by 2030, marking a major shift in the country’s climate policy. Most recently, the country’s updated Nationally Determined Contribution (NDC), released in September 2025, promised that global greenhouse gas emissions would fall 7–10% below peak levels by 2035.

At the same time, the sector is also facing increasing financial pressures and increased scrutiny from global markets. Constant capacity, unstable profits and the rise of energy consumption increase credit risks within the industrial sectors, while the recent increase in exports is reorganizing the global trade of steel and contributing to renewed trade conflicts with major foreign countries.

Against this backdrop, the industry is now facing a growing challenge of trust on many fronts. Progress toward the transition to crude steel has fallen short of policy expectations, financial stability is under pressure, and expanding imports are fueling trade tensions with key partners.

Together, these trends raise a broader question: whether China’s steel sector can simultaneously deliver on its ambitions, maintain financial stability, and maintain constructive relationships with global markets. Restoring credibility will require structural reforms that align climate commitments and fiscal discipline with the changing dynamics of global trade.

Important findings

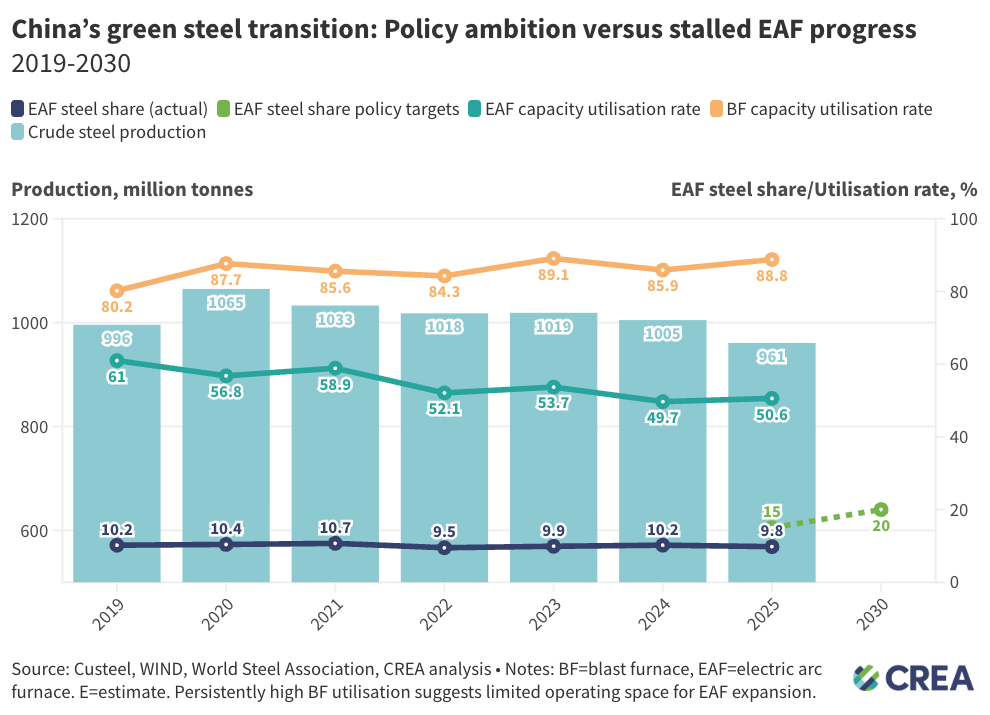

- Declining demand, rather than a structural shift to green steel, has driven emissions reductions in China’s steel industry by 2025. Neutral steel production fell below 1 billion tonnes (-4.4% YoY) for the first time since 2020, a larger than expected reduction from the policy framework.

- Reviving the ambitions of green steel requires a change in structure from the powerful carbon-base-basic oxygen furnace (BF-BOF). Increasing the share by 15-20% by 2030 could reduce BF-BOF steel production by 80-120 Mt, which is equivalent to Japan’s annual steel production and approaching that of India.

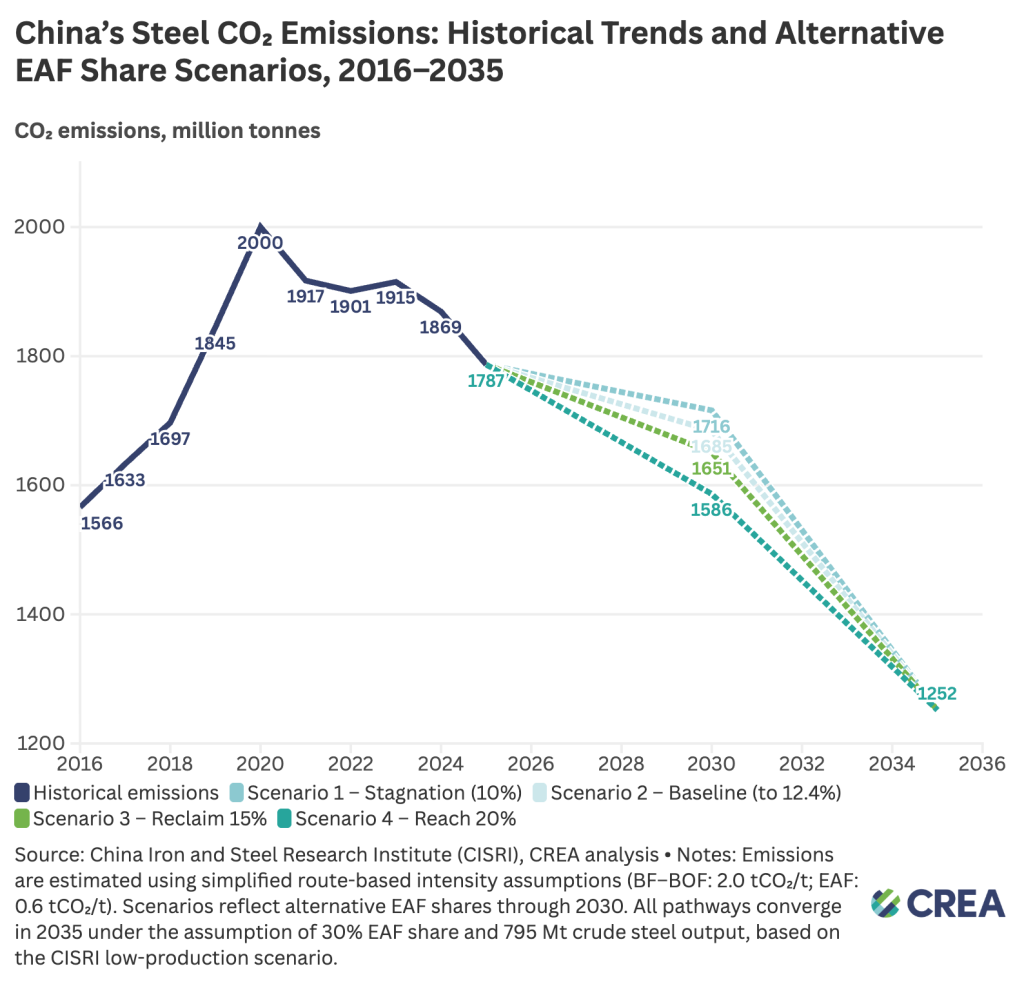

- The rate of steel can greatly exceed national standards. Under the EAF-led reform, steel industry production, which increased in 2020, could drop to around 37% below peak levels by 2035, far exceeding China’s revised Nationally Determined Contribution (NDC) target of a 7-10% reduction in economy-wide emissions.

- Unrelenting capacity and weak domestic demand have severely damaged profits in China’s steel sector, with industry debt rising to more than 1 trillion CNY (+20%) between 2020 and 2025. The EAF’s lead path of at least 20% by 2030 could support profits up to CNY 220-220% and reduce the value of assets by CNY 220 220 billion. moving the branch to a stable position.

- China’s share of world steel trade rose from 13.3% to 29.2% between 2020 and 2025, which increased its exposure to trade conflicts. Strengthening the role of green steel will be important for strengthening the global competitiveness of the sector, especially in the midst of strengthening trade measures related to carbon, such as the EU’s Carbon Border Adjustment Mechanism (CBAM).

Figure – China’s crude steel transition: Strategic ambition versus stalled EAF development, 2019–2030

Figure – China’s steel CO₂ emissions: Historical trends and some EAF sector trends, 2016-2035

China’s steel industry can strengthen its commitment to climate change, financial responsibility and global trade in the following ways:

- Coordinate climate, industry, and trade policies to strengthen green competitiveness.

- Accelerating the decline of the furnace reduces supply pressure, improves market conditions, and directly reduces the sector’s overall emissions.

- Increase the EAF share to 20% by 2030, along with strong economic incentives to accelerate structural reform in the sector.

- Strengthen financial support for underperforming steel producers and implement exit mechanisms.

#Regaining #confidence #Chinas #steel #industry #Climate #change #financial #stability #market #confidence #Center #Energy #Clean #Air #Research